Farm Financial Risk Management Series Part II: Introduction of Financial Systems for New and Beginning Farmers

ID

AAEC-115P (AAEC-297P)

EXPERT REVIEWED

EXPERT REVIEWED

There are many factors to consider before starting a new farm enterprise. Financial management is an important component in the startup and decision-making processes for beginning farmers. The purpose of this series of publications is to inform Virginia agribusiness owners and managers about the farm financial risk management tools, techniques, and resources available to help them prepare and use a financial systems approach for their operations.

This publication introduces the four financial statements that farm managers can use to record and assess historical farm financial performance. The topics covered in this resource are not all-inclusive, but after reading this publication, beginning farmers should be prepared to move forward in planning for their farms.

The accompanying parts in the series include “Farm Financial Risk Management Series Part I: Overview of Financial Statements for New and Beginning Farmers” (Virginia Cooperative Extension publication AAEC-114P (AAEC-296P)), and “Farm Financial Risk Management Series Part III: Introduction to Farm Planning Budgets” (VCE publication AAEC-116P (AAEC-298P)). A compilation of excellent resources that includes examples, how-to videos, and training resources is included in the appendix at the end of this publication.

For questions about this or other farm startup topics, contact the local Virginia Cooperative Extension office or visit the Virginia Beginning Farmer and Rancher Coalition Program website at www.vabeginningfarmer.org.

Farm Financial Statements

A complete farm financial system comprises four financial statements and four planning budgets. The four financial statements — balance sheet (or net worth statement), cash flow statement, income statement, and owner’s equity statement — are used to record financial details. Preparation of each statement requires access to detailed data on farm enterprises, production methods, sources of farm revenue, costs for each enterprise, equipment and facility conditions, inventory of supplies, sources of off-farm income, and insurance and tax records. While the effort required to compile these records might initially require several hours of time, it is important to note that this information is used to build both the financial statements and the planning budgets.

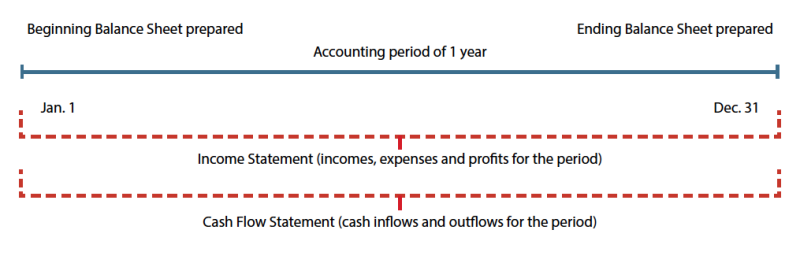

A key component to each of these four financial statements is the time frame within which each piece of farm data is collected and entered into the financial system. In general, most financial statements are prepared annually and include farm records from the previous calendar year. Each statement provides a mathematical record that demonstrates the farm operation’s ability to meet both short- and long-term financial goals. When constructing farm financial statements, consider using a timeline (fig. 1) to focus attention on the time measurement noted within each statement.

The balance sheet (or net worth statement) and the owner’s equity statement present two annual “snapshots” of the farm’s financial standing on the first and last days of the year. The income statement portrays a “video” of farm revenues and expenses as recorded throughout the year. The cash flow statement includes monthly pictures of the farm’s checking account balances. In combination, these four statements provide the manager with information on changes in the farm’s financial situation at varying levels of detail.

Balance Sheet

A balance sheet is a systematic listing of all a business owns (assets) and all that it owes (liabilities) at a specific point in time; it is also referred to as a net worth statement. Completion of the balance sheet provides detailed analysis of three key components of the business:

- Assets owned by the farm.

- Liabilities owed by the farm.

- The difference between assets and liabilities.

Armed with this information, the farm manager can use the balance sheet to assess and compare the annual net worth of the farm business from its initial establishment to the end of the previous year.

The balance sheet includes a classification for each of the farm’s assets, according to their liquidity, or the farm’s capacity to generate cash quickly and efficiently to meet its financial commitments as they fall due. The balance sheet is typically constructed at the beginning and the end of each calendar year. Therefore, the balance sheet serves as a snapshot in time at these two points in the life of the business.

Itemize Assets Owned by the Farm

Current farm assets include all items whose values will likely be realized in cash or used up during the normal course of business each year, and include

- Checking accounts.

- Notes and accounts receivable.

- Hedging accounts with commodity brokers.

- Prepaid expenses.

- Market livestock.

- Crops on hand that will be converted to cash during the operating cycle of business.

- Supply inventories - feed, fertilizer, seed, and other farm supplies.

Noncurrent farm assets are expected to yield services to the business over multiple years and can include

- Machinery and equipment.

- Breeding livestock.

- Buildings.

- Other types of real estate.

- Retirement accounts.

- Water-handling facilities - irrigation, tile.

- Residence.

- Various improvements - establishing orchards; controlling brush; adding and repairing fences, roads, ponds; etc.

Itemize Liabilities Owed by the Farm

Current farm liabilities are existing obligations that the farm is expected to pay in the next 12 months. They include

- Accounts payable to merchants and supplycompanies.

- Notes payable to lending institutions.

- Accrued expenses - expenses that have beenincurred but have not been paid because of theirstatement date, such as interest, taxes, rent, and leasepayments.

- Current portion of all term debt - the amountof principal on all term debt due within next 12months.

Noncurrent liabilities are farm business obligations that have a maturity date later than 12 months and include the noncurrent portion of notes payable on real estate and non-real estate farm assets.

What’s the difference?

A balance sheet allows farm owners and managers to determine the overall farm net worth — or owner’s equity — by calculating the difference between total farm assets and liabilities. More details on the statement of owner’s equity are provided in the next section of this publication.

How do farm managers assess information on balance sheets?

In addition to determining the overall farm net worth at the beginning and end of the accounting period, the information on a farm balance sheet can be used by farm managers to determine the short- and long-term capacity of the business to receive loans and make the payments. Liquidity of the farm is defined as the ability to meet obligations as they come due in the short term. Farm business liquidity is calculated as the difference between current assets and liabilities. For example, if a liquidity problem is discovered, farm managers can choose to address this financial risk in one or more of the following ways:

- Refinance current debt to secure lower payments.

- Slow farm expansion until liabilities are reduced.

- Reduce overall annual operating debt.

- Liquidate farm assets and use the cash to pay downdebts.

- Reduce annual costs of operating the farm business.

- Improve overall farm profitability by increasingyields, reducing expenses, or finding new marketsthat offer higher prices.

Solvency of the farm is defined as the ability to meet long-term financial obligations and cover fixed expenses. Farm business solvency is calculated as the difference between total assets and liabilities. Using the relationship between total assets and liabilities over different points in time provides farm managers with the information needed to achieve long-term growth and profitability goals. For example, if a solvency problem is discovered, farm managers can choose to address this financial risk in one or more of the following ways:

- Retain additional net farm income in upcomingyears.

- Reduce overall debt owed by the farm business.

- Sell farm assets to reduce debt.

- Improve overall farm profitability by increasingyields, reducing expenses, or finding new marketsthat offer higher prices.

Income Statement

An income statement is a summary of the revenue (receipts or income) and expenditures (costs) of the farm business over a specified period of time. The income statement is also called a “profit and loss statement.” The purpose of the income statement is to measure the difference between farm revenues and operating expenses incurred over a period of time and to allow for direct calculation of net farm income. Construction of the income statement allows farm owners and managers to answer another key financial risk management question: Did the business demonstrate a net income that was positive (farm earned a profit) or negative (farm lost money) last year, and how large was the profit or loss?

Income statements are typically constructed at the end of each operating period, and they represent revenues, expenses, and net income incurred as a result of undertaking farm operations. Therefore, the income statement demonstrates the “bottom line” of the farm business over a specific time period.

The first components listed on the income statement are farm revenue streams. Revenues are calculated by multiplying the number of units sold by the price received per unit by each enterprise during the previous accounting period. Farm revenues can be recorded in any of the following forms:

- Cash - dollars earned from every commodity produced and sold.

- Noncash - inventory produced that is not yet sold and any accounts receivable due to the farm.

- Gain or loss on sale of capital assets.

- Nonfarm adjustments - off-farm income, custom work, government payments, etc.

What did the farm business SPEND last year?

The second component listed on the income statement is farm expenses, which includes all expenses incurred from operations carried out on the farm during an accounting period. Farm expenses are calculated by multiplying the price of the input by the number of units of input used during farm operations. Expenses can be recorded in any of the following forms:

- Cash - dollars spent on feed, seed, fertilizer, fuel, market livestock purchases, farm labor, insurance premiums, veterinary bills, etc.

- Noncash - depreciation, accounts payable, accrued interest, accrued expenses (property taxes), and adjustments for prepaid expenses.

It is important to note that principal payments on loans are not included as an expense on the farm income statement because the loan principal is NOT considered an expense.

How do farm managers assess information on income statements?

Income statements serve as a starting point for analyzing profitability of the business over a specific time period because the data included on the form show whether the farm business had a profit or loss last year. Calculation of net farm income from operations is found by subtracting total expenses from total farm revenues earned during the prior accounting period (typically a calendar year). To calculate net farm income, subtract any gains or losses (e.g., sales of capital assets) from net farm income from operations.

If the income statement reveals that the farm earned a positive net income over the time period, the farm owner or manager has the opportunity to use these profits to fund one or more of the following:

- Pay family living expenses and other needed cash withdrawals.

- Pay income and social security taxes.

- Increase cash reserves or purchase needed farm assets.

- Reduce liabilities through payment of loan principal balances or other accounts payable.

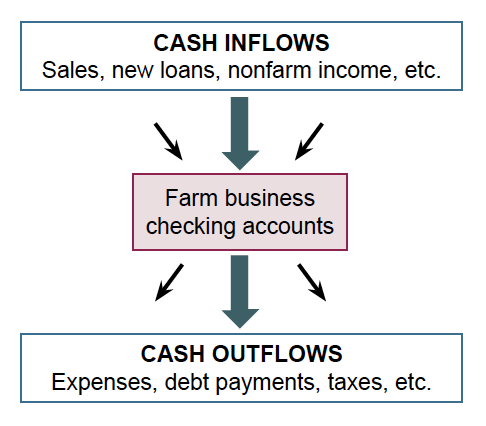

Statement of Cash Flow

A statement of cash flow is a listing of cash flows that occurred during the previous accounting period. The purpose of the cash flow statement is to show how cash entered and exited the business. Construction of the statement of cash flow allows the farm manager to follow the amounts and timings of cash movement in and out of farm checking and savings accounts (fig. 2).

The statement of cash flow is typically constructed at the end of each operating period; it uses and reorders the information from the balance sheet and income statement. The statement of cash flow demonstrates the net increase or decrease in cash over a specific time period.

Components of the Statement of Cash Flow

- Cash from operating activities - farm income and expenses.

- Cash from investing activities - farm sales or purchases of assets.

- Cash from financing activities - new borrowed capital, loans received, principal repayment, and gifts and/or inheritances received.

Nonfarm income and expenses (in cases where the business is classified as a sole proprietor) and beginning and ending cash on hand can also be included on the statement of cash flow. However, it is important to note that depreciation is not included because this is considered a noncash expense.

How does information on a cash flow statement aid farm managers in decision-making?

In agriculture, cash flow is usually inconsistent because costs are incurred at the beginning of and throughout the production season, and revenues are received only at the time of harvest or market sales. Often a farm business can be profitable (according to the income statement) and still have several months with negative cash flow. It is important to recognize that a statement of cash flows does not show overall farm profitability and demonstrates the need to complete all four financial statements to manage farm finances.

A key financial risk management strategy used by farm managers is to construct a monthly statement of cash flows to determine when and where funds are needed to meet repayment obligations of the business in the short, intermediate, and long terms. Also, farm managers can take advantage of periods of positive cash flow to obtain discounts on input purchases by using the information in the cash flow statement to plan ahead. Finally, farm owners can benefit in tax planning by identifying and taking advantage of income tax benefits resulting from better timing of purchases, sales, and capital expenditures.

Statement of Owner’s Equity

A statement of owner’s equity reconciles the owner’s equity (or farm net worth) stated at the beginning time period with the owner’s equity remaining at the ending time period. The purpose of the statement of owner’s equity is to calculate the value of the business after the total claims of creditors are subtracted from the asset value. The term “owner’s equity” refers only to the farm business, and this financial statement includes no information for individuals. Construction of the statement of owner’s equity allows the farm manager to determine which of the three components (contributed capital, retained earnings, or market valuation) caused changes in the net worth of the farm business last year. Like the balance sheet, the statement of owner’s equity is typically constructed at the beginning and the end of each calendar year and serves as a snapshot in time at each of these two points in the lifetime of the business.

Components of the statement of owner’s equity include the following:

- Change in contributed capital - Capital contributed to the business by its owner, such as any personal cash or property the owner used to start the business or has contributed since that time. The value of contributed capital should remain the same on any future balance sheets.

- Change in retained earnings - Earnings or business profit that has been left in the business rather than withdrawn, such as any before-tax income not used for family living expenses, income taxes, or other purposes. Retained earnings are typically recorded in the form of additional assets (not always cash), decreased liabilities, or some combination of both. Retained earnings are expected to increase for any year where net farm income exceeds the combined total of income taxes paid and withdrawals for family living expenses.

- Change in market valuation - Any change caused by fluctuations in market values when market valuation — rather than a cost basis — is used. If inflation is high, land market values could increase due to land ownership as opposed to resulting from farm production. Market valuation makes it easy to analyze what part of total equity is the result of valuation differences.

Additional Resources and Information

Ag Risk & Farm Management Library - https://agrisk. umn.edu/library

Center for Farm Financial Management, University of Minnesota - https://www.cffm.umn.edu/.

Farm Finance, Safety Net, and Risk Management, National Sustainable Agricultural Coalition - http://sustainableagriculture.net/our-work/issues/credit-safety-net-programs/.

Harwood, J., R. Heifner, K. Coble, J. Perry, and A. Somwaru. 1999. Managing Risk in Farming: Concepts, Research, and Analysis. U.S. Department of Agriculture, Economic Research Service. Agricultural Economic Report No. AER774. Washington, DC: USDA ERS.

Kay, R. D., and W. M. Edwards. 1994. Farm Management. 3rd ed. New York: McGraw-Hill.

New Farmers, U.S. Department of Agriculture - https://newfarmers.usda.gov/.

O’Brien, D., N. D. Hamilton, and R. Luedeman. 2005. “Risk Management.” In The Farmer’s Legal Guide to Producer Marketing Associations, 67-82. Des Moines, IA: Drake University Agricultural Law Center. https://nationalaglawcenter.org/wp-content/uploads/assets/ articles/obrien_producermarketing_ch6.pdf.

Risk management resources, U.S. Department of Agriculture Economic Research Service -

www. ers.usda.gov/topics/farm-practices-management/risk-management/.

For more information about preparing and analyzing farm financial statements in Virginia, please contact John Bovay at bovay@vt.edu. For more information and resources directly aimed at beginning farmers, visit the Virginia Beginning Farmer and Rancher Coalition Program at www.vabeginningfarmer.org.

Acknowledgements

The Virginia Beginning Farmer and Rancher Coalition Program is a statewide, coalition-based extension program. The program is housed in Virginia Tech’s Department of Agricultural, Leadership, and Community Education and is a program of Virginia Cooperative Extension. The Virginia Beginning Farmer and Rancher Coalition Program is sponsored by the Southern Extension Risk Management Education Center and the Beginning Farmer and Rancher Development Program of the USDA National Institute of Food and Agriculture, Award No. 2015-70017-22887.

Disclaimer

Although the authors have made every effort to ensure that the referenced URL links stated in this document are correct at time of publication, the authors do not assume that the referenced URL links will remain correct over the duration of time this document is in circulation and hereby disclaim any liability to any party for any loss, damage, or disruption caused by present and future errors or omissions, whether such errors or omissions result from negligence, accident, or any other cause.

Appendix

Following is a compilation of sources, examples, documents and how-to videos to help farm owners and managers organize farm records and complete farm financial statements and planning budgets.

Virginia Cooperative Extension materials are available for public use, reprint, or citation without further permission, provided the use includes credit to the author and to Virginia Cooperative Extension, Virginia Tech, and Virginia State University.

Virginia Cooperative Extension is a partnership of Virginia Tech, Virginia State University, the U.S. Department of Agriculture (USDA), and local governments, and is an equal opportunity employer. For the full non-discrimination statement, please visit ext.vt.edu/accessibility.

Publication Date

September 23, 2022