How to Make Your Money Go Further

ID

AAEC-216P (AAEC-334P)

EXPERT REVIEWED

EXPERT REVIEWED

Introduction

What do you have to show for the money you make each month? Do you have good health, a car, a home, and money in a savings and retirement account? Or do you seem to have a pile of debts and few assets?

The way you spend your money today will determine what money you have in the future. You can take steps now to control your financial destiny! Successful money managers make decisions daily that determine how they spend their money and how they use money to accomplish the things that are important to them. This publication provides some proven methods to help you become a good manager of your money and even to find the extra money you have to reach your goals.

You have control over the way you spend your money. You may choose to live below your income and build savings after meeting your regular monthly expenses. Living within your income and building a secure future requires careful planning, self-discipline, and the ability to say no to spending that doesn’t fit your personal finance goals.

The ability to manage money is something everyone has the opportunity to learn. In time, you will be able to develop the abilities that you begin to practice on a daily basis. We have just eight simple steps for you to follow in order to build successful money management skills:

- Clarify values.

- Set goals.

- Organize.

- Decide.

- Implement.

- Control.

- Evaluate.

- Monitor, review, revise.

Following these eight steps will help you plan a personalized spending strategy to reach your financial goals.

1. Clarify Values

What things in your life are most important to you? Your values determine the things you are willing to work hardest for. We have values in all areas of our lives including education, health, family, social, and many more. You might change some of your values depending on the circumstances, while you could be unwilling to change or compromise others. It is also possible that your values change over time as outside influences and personal development occurs. A few of the ways we develop our values are from our parents, peers, experiences, religion, the culture in which we live, and the media.

2. Set Goals

What are some things you want to accomplish during your lifetime? What will they cost? If you decide to put a plan in place to achieve these goals, you will be able to watch yourself move closer to these goals daily.

Good money management begins with goal setting. Goals give you direction. Goals motivate and encourage you as you work toward the things that are important to you. Some advantages of goal setting include:

- Provide direction and purpose.

- Encourage self-understanding.

- Identify needed changes.

- Improve self-confidence.

- Improve planning.

- Define priorities.

- Help guide decision-making.

As you begin to set goals, it is important to distinguish between wants and needs. For many people, the definitions of these terms get blurred. A need is something that is a basic necessity for survival. Examples of needs include food and shelter. A want is something desirable that will make your life more comfortable or enjoyable. For example, food is a need, but a dinner at an expensive restaurant would be a want.

How do you set goals? First, consider your values for you and your family. Review the list below. Pick out the things you and your family feel are most important and place a 1 beside them. Place a 2 beside the things that are somewhat important. Place a 3 beside the things that are not very important to you and your family.

____ Charity

____ Education

____ Family vacation

____ Clothes, shoes, makeup, hair care

____ Culture (theater, movies, plays, dance, recitals)

____ Start a new business

____ Personal appearance

____ Save money

____ Job success

____ Food

____ Insurance

____ Friends

____ Recreation

____ Boat, fishing equipment

____ Household furnishings

____ Transportation, car, truck, cycle

____ New house, condo, apartment

____ Health

____ Family activities

____ Make lots of money

____ Pay off debts

____ Jewelry

____ Entertainment

____ Other

Ranking your values as an individual can be difficult. It can be even harder when two or more people live together and share money. It can be difficult to discuss how money should be spent, but it is important.

Setting these priorities will help you determine what to work toward. For example, if you placed a 1 beside a new car, your goal may be to buy a new car.

However, goal setting involves more than simply deciding what’s important to you. To help identify goals, ask yourself these questions:

- What do I want to do with my money?

- How much will it cost?

- How long will it take me to reach that goal?

Make a list. Use a pencil and paper or your computer to write down what you want to do with your money.

Next, it is time to create SMART goals. SMART is an acronym for Specific, Measurable, Adaptable, Realistic, and Time-bound.

Specific – Make your goals as specific as possible. The more specific your goals, the easier it is to work toward them. Saying “I want financial security” is not very specific. Ask yourself what it takes to be financially secure. Your answer might be to have $20,000 in savings when you retire at 65. This is a specifically defined goal.

Measurable – Make sure that your goals are measurable so that you can see your progress. Perhaps, in order to achieve your retirement goal, you will need to deposit $75 every month into your savings account. Measure your progress by looking at your balance changes over time to see how it compares to your end goal.

Adaptable – Know that it is OK to change your goals. Along the path to completing your goal, your values or objectives could change. Perhaps your goal was to purchase a home two years from now, but an unexpected career change caused you to move to a new community. Depending on the housing market and your expected career changes, your housing goal might need to change.

Realistic – You want to make sure your goals are realistic and reachable. If your goal requires you to save $1,000 every month but you can only set aside $100 every month, your goal is not realistic. Instead, alter the goal to save $100 monthly. You might need to extend the length of time you are saving, lower the dollar amount of your end goal, or a combination of both.

Time-bound – Include a time period for your goal and specify when you plan to reach your goal. For example, how many years away is your retirement goal of $20,000? The time period you assign to your goal will greatly impact the amount of money you need to save to reach your goal.

Here is an example of a SMART goal. “I plan to reach my savings goal of having $20,000 in my account when I retire 20 years from now. To accomplish this, I will deposit $75.31 every month into my savings account that earns 1% interest for the next 20 years.”

Your goals should be yours. They need to fit your life; no one else can set your goals for you. You will be much more likely to reach your goals if they are things you really want. Goals will be different for each individual and family.

Picture your goals in your mind. Imagine living in that new house or going on that vacation. Creative daydreaming puts your goals into your subconscious mind. You can even print a picture of your goal and post it somewhere you will regularly see it. Once this happens, you will start thinking of ways to reach that dream. You will automatically see ways to make your dream a reality. Envision the exact things you want.

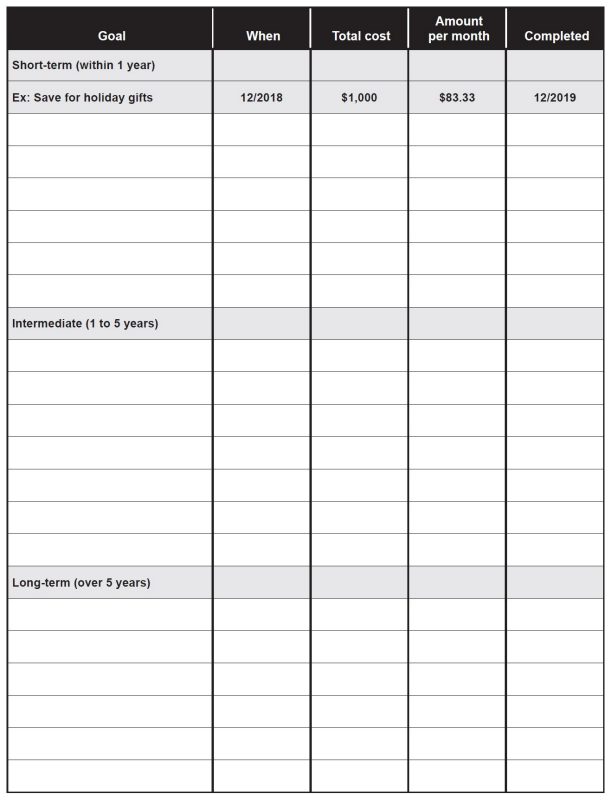

Divide goals into three categories — short-term, intermediate, and long-term — and write them on Worksheet A.

- Short-term goals are the things you want to get done in a year or less.

- Intermediate goals are things you want to accomplish in the next one to five years.

- Long-term goals are things you want to achieve in the next five years or more.

As you list your goals, decide which goals you want to achieve first. As you set dates for reaching your goals, ask yourself which goals are the most important and which are the least important. Ask yourself:

- How important is this for me and my family?

- How urgent is this? Paying $1,000 worth of taxes that are due tomorrow is more urgent than paying off $950 in credit card debt.

- What will happen if you don’t work on this goal? If you owe a $700 credit card bill, paying off $100 per month will cost you less in interest than paying $35 a month. It may squeeze your budget to pay $100 per month, but it will save you money.

- What will it take in terms of money, time, energy, skills, knowledge, and ability to reach this goal? Goals are important keys to successful money management. They will help you achieve your dreams within your set period of time.

3. Organize

An organized, dedicated financial space will help you manage your family financial matters better. Keep all bills and important papers in one location. This location could be a digital or physical location. In this space, create a home filing system consisting of family, property, and financial records. When you receive any bill, important letter from a creditor, or financial statements from your bank, credit union, or other financial institution, put the correspondence in your home filing system. Digital copies of these items can be filed on your computer. If you and a creditor disagree about how much you owe or the way you pay your bills, you have your own records to prove what has happened.

Your dedicated financial space can be elaborate or simple. The type of filing system doesn’t matter as long as you have some way to organize your financial information and history. Papers can be separated using large envelopes or individual file folders in a file box or cabinet, or by storing them on your computer or online. Folders with pockets could be used to store loose-leaf papers.

Label file folders according to the types of records kept in each section. For example, labels may be as follows: net worth statement (what you own versus what you owe), record of earnings, record of expenditures, legal records, health records, real estate records, family papers, household inventory, employment records, automobile, housing, utilities, credit card and installment payments, insurance, tax records, and general household information. If you have multiple credit cards, separate documents for each card to make them easy to find.

4. Decide

How much money do you have to spend each month to meet basic living expenses and how much do you have to put toward your goals? The money you spend each month usually comes from:

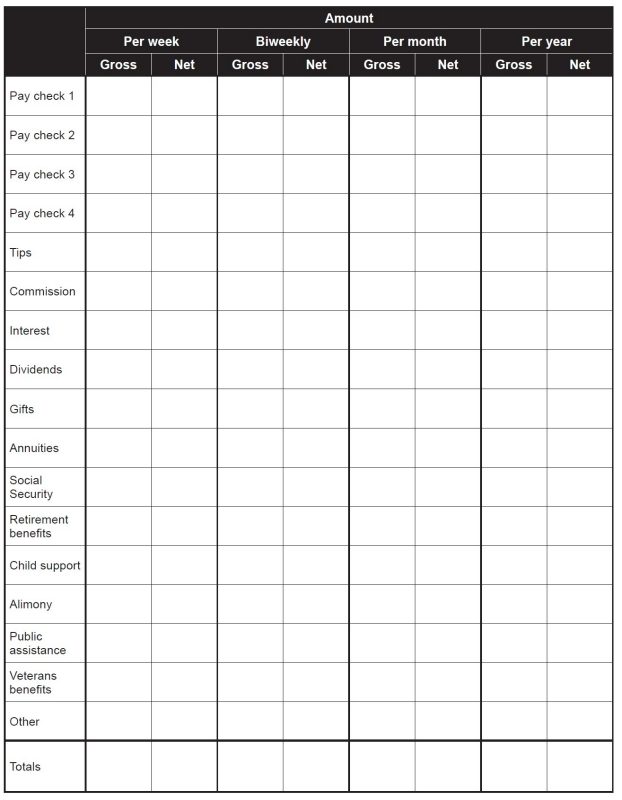

- Earnings from wages, salary, tips, commissions, rental income, interest, dividends, capital gains from the sale of an asset, or retirement benefits.

- Money received from relatives, friends, or the government in the form of transfer payments (such as SNAP benefits or Social Security).

If you already have a household cash flow statement (refer to Virginia Cooperative Extension publication AAEC-185NP, “Your Financial Health – Cash Flow Statements”), you can refer to it for information on your income. If not, use Worksheet B to help you list your sources of income.

Calculate your monthly disposable income. First, determine how much you want to spend each month.

- Find your most recent pay stub.

- Look at the amount of gross pay — the amount of money you earn before deductions.

- Look at the amount of money going to each deduction. What percentage of your gross pay goes to each deduction?

- Look at the amount of your take-home pay. Also known as net pay, this is your gross income minus your deductions.

- Your total disposable income is your take-home pay plus money from other sources.

If you have an irregular income, using a recent pay stub may not be as helpful. Instead, estimate the total you expect to make for the entire year and divide by 12. Keep your estimate low. Examples of workers who may have irregular incomes include car salespeople, farmers, artists, writers, and restaurant servers.

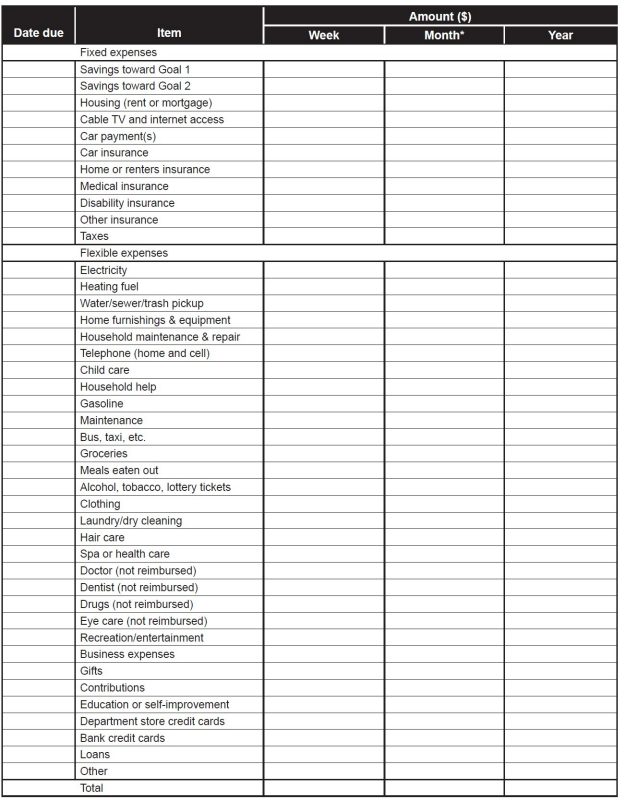

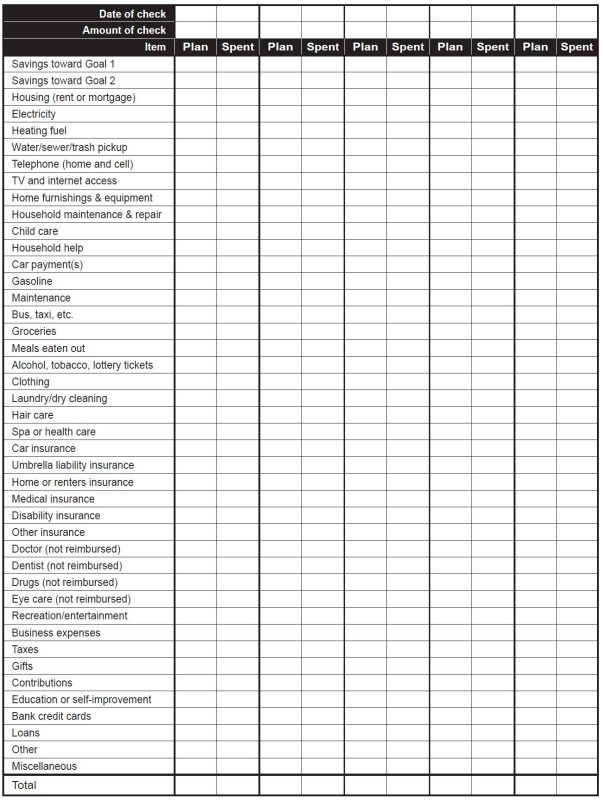

Next, make a spending plan for each month that records how much money you will spend on each expense category. To do this, determine how much money you spend on food, housing, transportation, clothing, personal care, medical care, and other things. If you don’t know how much you spend each month for these items or you have a cash flow statement to remind you, you should write down everything you spend every day to track your expenses. Do this for at least one month but ideally for two to three months. When you make a purchase, write down the amount. Use Worksheet C to help you see where you are spending your money. Be sure to include things you pay for with cash.

After you have a written record of where your money is going, divide your spending into categories: fixed, flexible, and periodic expenses. Spending can also be divided into daily, weekly, monthly, seasonal, or yearly expenses. Know what type of expenses you have and when and where you spend money. You can build a sound money management program using these methods.

Fixed expenses are the budget items you pay a specific amount of money for every month for a certain period of time. These obligations are usually enforced through a signed contract. Some examples are rent or mortgage payments, life insurance, car insurance, home insurance, and installment payments such as your car loan. When looking at these examples, if you have some of these expenses, but don’t pay them monthly, they would be periodic expenses.

Flexible expenses are the budget items you have more control over. You decide how much you will buy and how much you will spend. Flexible expenses include food, clothing, gas, electricity, water, transportation, gasoline, car maintenance, personal care, furnishings, household expenses, and professional expenses.

Periodic expenses are irregular or seasonal expenses that occur infrequently and are easily overlooked when developing a spending plan. Examples may be annual property or real estate taxes, auto inspection fees, and tuition, certain insurances, and school expenses.

We spend some money on a daily basis and some on a monthly, quarterly, semiannual, or annual basis. Write down when expenses are due on Worksheet D. Then set aside enough money to cover an expense when it comes due.

Once you know where your money is going, use Worksheet E to help you plan your monthly spending. Start by writing down the amount of money you have to spend each payday.

5. Implement

The implementation phase involves putting the plan into action. As income is received and expenses occur during a given time period, determine totals for the time-period.

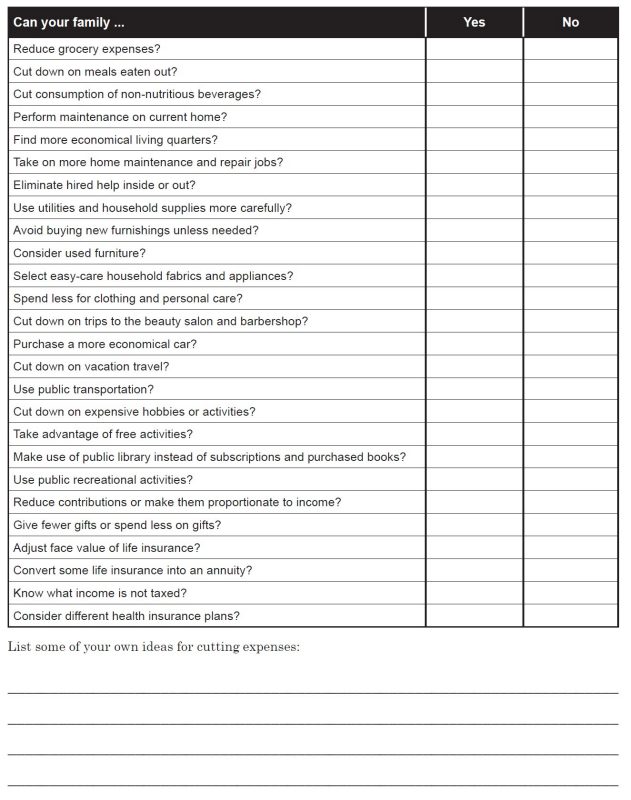

Use this information to manage cash flow and make savings, investing, and purchasing decisions. Use the information from Worksheet C to figure out your monthly expenses. Then compare them to some spending guidelines, such as those in Table 1. This data — plus your record of expenses — can help you decide how much to spend each month. You can use Worksheet F to identify some ways to adjust your spending. Table 2 is provided to give you an idea of the average spending patterns of households that spend around $47,000 per year. The information in Table 2 should NOT be used as a guideline. Important to note, that the Bureau of Labor Statistics does not include saving in their expense numbers.

On Worksheet E, write down how much you would like to spend for each item. As you develop your plan, see if you have allowed money for the following items:

- Major expenses and future goals such as adding rooms to your home, buying a car, braces for your children’s teeth, paying for your child’s education, buying a boat, gifts, or furniture.

- Emergencies such as medical expenses, car accidents, unemployment, car repairs, dental bills, house repairs, and appliance repairs.

- Periodic expenses.

- Debts or past-due bills.

- Monthly expenses such as savings or investments, rent or mortgage, utilities, household supplies, food, contributions, installment payments, and prescription and over-the-counter medications.

- Daily expenses such as school lunches and supplies, tobacco, snacks, and meals out.

- Entertainment and recreation.

Write down how much you plan to spend throughout the pay period. Try to stick with your plan through this pay period. Remember to write down how much you spend and what you bought. Use those figures to calculate your actual spending so that when you start the next pay period, you can compare what you planned to spend with how much you actually spent. Then plan for how you will spend your next paycheck.

6. Control

Control requires you to select a variety of methods and techniques to keep income and expenditures on target.

Stick to your spending plan. Now that you have a written plan for what you will spend each pay period, stick to it! Before you spend your next dollar, ask yourself these questions:

- Will this purchase help me reach my financial goals? If your goals are important enough to you, they will motivate you to stick with your plan.

- Is this purchase listed on my spending plan?

- What will I have to give up if I spend my money on this purchase?

- Do I really need this new item, or do I need this money to buy groceries or gas?

- How many hours do I need to work to pay for this item?

Make your new spending and savings plan a part of your daily life. Look for ways you can spend less money. Start using your spending plan today, rather than putting it off until tomorrow. Tell someone else what you’re trying to do so they can encourage you along the way.

• Take advantage of every opportunity to break old buying habits and encourage new ones. Continuously look for ways to reduce your spending.

• Do something every day that will help you save money. You could cut one coffee break at work. You could take your own instant coffee to work rather than buying coffee at the company cafeteria.

• Finally, develop a reward system for successfully following your spending plan. Choose a reward that will not sabotage your spending plan. If your reward will cost money, then save up to pay for it.

7. Evaluate

Evaluation is a continuous and essential process that provides feedback for determining if the plan is working. If your actual expenses have exceeded the category amounts, then you must reexamine categories and clarify goals.

Don’t let an exception get in the way of your new spending plan. If you start taking your lunch to work to cut food expenses, eating out one day may discourage your new habit and keep you from reducing your food bill. It will slow your ability to reach your goal. Be your own mentor and avoid tempting situations. However, remember that changing your spending habits takes time. If you backslide into old habits, learn from the experience.

8. Monitor, Review, Revise

Practice your spending plan for a few months and then look it over. If you put $100 in savings at the first of the month and had to take out $50 before the end of the month, you might only be able to save $50 a month. That’s OK; the plan needs to work for you. At least you know what you are able to save. Reviewing spending helps you decide exactly how much you should spend and save.

Review your spending plan regularly and revise it so it works for you. Here are some questions to ask yourself when deciding where to spend your money:

- Is this the best use of my money right now?

- Will this purchase help me reach my financial goals?

- Is there something else I need to use this money for?

If you have trouble reaching your goals, you might want to reevaluate them. Are they truly important to you? Is another family member or friend interfering with your ability to reach your goal? A sincere commitment and dedication to your spending plan will help you manage your money better.

Summary

Take control over where your money goes, instead of letting it control you. Envision your dream, write it down, follow your plan, and you will be guiding your money to where you want it to go.

Build a sound money management program by:

- Getting organized.

- Setting goals.

- Creating a spending plan.

- Knowing your income.

- Knowing your expenses.

- Following your monthly spending plan.

- Deciding to stick to your spending plan.

- Evaluating your spending plan and adjusting as needed.

Remember, what you have in the future depends on what you do with your money today.

Worksheet A. Family Goals

Worksheet B. Income

Worksheet C. Expenses

Note: Some expenses (for example, telephone and child care) can be fixed or flexible.

*To calculate monthly expense, multiply the amount per week by 4.3

Worksheet D. Periodic Expenses

Write down expenses due throughout the year. Add up the totals from each month and divide by 12 to find your average periodic expenses.

Worksheet E. Paycheck Planning Sheet

Worksheet F. The Balancing Act

Family spending must often be adjusted to stay within income limits. Take a few minutes to complete the exercise below.

| Item | Percentage | Example* (take-home pay for a family of 4 = $2,500/month) |

|---|---|---|

| Housing (including utilities and supplies) | 33-35% | $825-875 |

| Food | 18-25% | $450-625 |

| Transportation (fuel/public transportation) | 7-9% | $175-225 |

| Clothing | 6-12% | $150-300 |

| Medical (including dental, prescriptions, health insurance) | 6-8% | $150-200 |

| Car insurance | 2-3% | $25-50 |

| Life insurance | 2-5% | $50-125 |

| Educational advancement | 1-2% | $25-50 |

| Credit obligations (including auto payment) | 12-15% | $300-375 |

| Savings | 2-10% | $50-250 |

| Recreation/entertaiment | 2-6% | $50-150 |

Source: Adapted from: American Consumer Credit Counseling, Community Spending Guidelines, Retrieved March 2019.

Note: Necessary living expenses (shelter, food, clothing, and transportation) account for more than half of pretax income.

* This is only one example. Each family’s situation will be different.

| Item | Percentage* | Monthly | Annually |

|---|---|---|---|

| Housing | 39.0% | $1,529 | $18,348 |

| Food | 14.2% | $555 | $6,660 |

| Transportation | 16% | $647 | $7,764 |

| Apparel and services | 2.6% | $100 | $1,200 |

| Health care | 9.5% | $371 | $4,452 |

| Personal insurance and pensions | 4.3% | $170 | $2,040 |

| Education | .9% | $37 | $441 |

| Reading | 0.2% | $6 | $72 |

| Personal care products and services | 1.3% | $49 | $588 |

| Cash contributions | 3.0% | $118 | $1,416 |

| Tobacco products and smoking supplies | 0.9% | $34 | $408 |

| Alcoholic beverages | 0.7% | $29 | $348 |

| Miscellaneous | 1.7% | $66 | $792 |

| Entertainment | 5.3% | $209 | $2,508 |

| Total | 100% | $3,920 | $47,037 |

Source: Author’s calculations are based on the Consumer Expenditure Survey, U.S. Bureau of Labor Statistics, September 2023.

* Average share of take-home pay spent on major spending categories.

This publication was based on a publication revised by Celia Ray Hayhoe, Ph.D., CFP®, Family Resource Management Cooperative Extension Specialist, Virginia Tech, Blacksburg(Adapted from: Consumer Credit Counseling Service, Consumer Education Department of Atlanta)

Virginia Cooperative Extension materials are available for public use, reprint, or citation without further permission, provided the use includes credit to the author and to Virginia Cooperative Extension, Virginia Tech, and Virginia State University.

Virginia Cooperative Extension is a partnership of Virginia Tech, Virginia State University, the U.S. Department of Agriculture (USDA), and local governments, and is an equal opportunity employer. For the full non-discrimination statement, please visit ext.vt.edu/accessibility.

Publication Date

May 1, 2025