A Decision-Making Tool to Determine the Feasibility of Purchasing Virginia Milk Commission Base

ID

DASC-30P (DASC-111P)

EXPERT REVIEWED

EXPERT REVIEWED

Introduction

Dairy farmers are usually subject to net income fluctuations due to volatility in both milk and feed prices. Risk management tools, such as hedging milk prices in the futures market, may be used to protect dairy farmers against milk price volatility. Alternatively, dairy farmers selling milk in Virginia can buy Virginia milk commission base (MCB) to obtain higher milk prices and, therefore, sustain or increase net cash flows. A decision-making spreadsheet (http://pubs.ext.vt.edu/DASC/DASC-30/milk-commission-base.xlsx). was developed to help farmers evaluate the decision whether or not to purchase a certain amount of MCB to increase their net cash flows.

Milk Commission Base

Owning milk commission base entitles the producer to sell a specified amount of milk, usually in pounds, to a distributor or processor within a certain period of time. In turn, the distributor or processor agrees to purchase the specified amount of milk during that same period of time (Virginia Administrative Code 2008). Milk commission base gives the producer the right to sell milk at Class I prices, after certain discounts, equal to the amount (i.e., pounds) of MCB owned by the producer (Groover 2009).

As an example, consider a 220-milking-cow dairy farm in Virginia producing 5,000 hundredweight (cwt) of milk per month and owning 500 cwt of MCB (i.e., 10 percent of its total production). Assuming a net price of $22.75 per cwt for the MCB and $19.50 per cwt for the nonbase milk, the producer income would be equal to $99,125 per month (i.e., 500 cwt × $22.75 + 4,500 cwt × $19.50 = $99,125). Alternatively, if the producer does not own any MCB, its income would be $97,500 per month (i.e., 5,000 cwt × $19.50 = $97,500). By owning MCB, the producer’s net cash flow (excluding investment) would have increased by $1,625 per month.

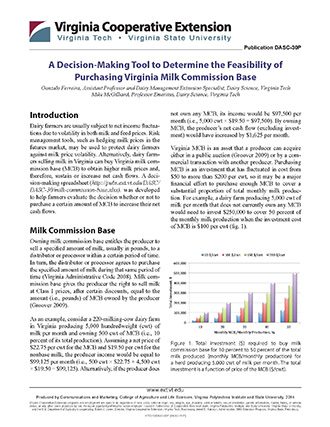

Virginia MCB is an asset that a producer can acquire either in a public auction (Groover 2009) or by a commercial transaction with another producer. Purchasing MCB is an investment that has fluctuated in cost from $50 to more than $200 per cwt, so it may be a major financial effort to purchase enough MCB to cover a substantial proportion of total monthly milk production. For example, a dairy farm producing 5,000 cwt of milk per month that does not currently own any MCB would need to invest $250,000 to cover 50 percent of the monthly milk production when the investment cost of MCB is $100 per cwt (fig. 1).

Don’t Use It and You’ll Lose It

Milk commission base is essentially a certificate to sell the stated amount of milk at a premium price each month, repeating every month (Groover 2009). Failure to sell that amount of milk monthly can result in penalties or loss of MCB. More specifically, producers must ship enough milk to cover their MCB during the months of September, October, and November. If a producer does not cover the total MCB, the missing amount of milk to be covered will be placed in an escrow account and the revenue from that base cannot be collected. During the months of September, October, and November of the following year, the producer must recover the entire MCB, including the portion in escrow. If this is not accomplished, the producer will lose that portion of the MCB forever.

Net Present Value

As for most investments, the suitability of buying MCB can be evaluated by the net present value (NPV) of future cash flow benefits. This means that all future monthly net benefits are discounted to determine their value in today’s dollars (opposite of compound interest). When the NPV is positive (NPV > 0), it is profitable to invest in MCB. When the NPV is negative (NPV < 0), investing in MCB will not be profitable and an alternative investment should be pursued. When NPV equals zero, the investment will break even.

The decision-making tool, milkcommissionbase_VT.xlsx (www.dasc.vt.edu), was developed to evaluate the NPV of investing in MCB in Virginia. To make use of this tool, the user must consider the following four variables:

- The desired period over which to evaluate the investment (months).

- The purchasing price of MCB ($/cwt, one-time purchase).

- The price differential between MCB and nonbase milk ($/cwt, every month).

- The desired annual discount or interest rate for this investment (%).

Acquiring the purchasing price of MCB and the price differential between MCB and nonbase milk can be a challenge. A representative from a marketing cooperative may be the best resource to provide these inputs.

The period for which the investment will be evaluated needs to be determined by the manager. For this, the manager should consider the desired rate of return or interest rate for the investment, the purchasing price of MCB, and the price differential between MCB and nonbase milk. For example, assuming a $3 per cwt difference in milk price, an interest rate of 7 percent, and a purchasing price for MCB equal to $100 per cwt, then the break-even timeline would be 37 months (fig. 2).

This break-even timeline tells the investor or producer how much time will pass before the investment generates net cash flows equal to the investment cost, including interest. In financial terms, the break-even timeline reflects how much time will pass before the investment has an NPV greater than zero (fig. 3).

Another determinant of the period for which the investment will be evaluated is the period for repaying any borrowed money used to purchase MCB. It would be reasonable to seek a break-even period shorter than the loan period.

It is worth mentioning that these calculations are based on the assumption that the investment analysis does not consider the resale value of MCB. The decision to purchase MCB can be totally different if the resale value of MCB is considered in the analysis and will be discussed later in this article.

Risk Analysis

As with most investments, the potential profits from owning MCB are subject to uncertainty, and therefore, there is risk involved in this decision. In the example described above, a difference between milk prices of $3 per cwt was assumed, but what would be the situation if the differential milk price were less than $3 per cwt?

To understand the uncertainty and risk of buying MCB, a Monte Carlo simulation was performed and included in the spreadsheet. Data from a dairy farm in Virginia (fig. 4) show that the difference between MCB and non-base milk prices have been normally distributed with a mean equal to $2.80 per cwt and a standard deviation equal to $0.50 per cwt. Using this distribution, the estimated NPV was randomly simulated 1,000 times to estimate the likelihood of obtaining a beneficial economic result by investing in MCB (table 1). Although profit occurs at a differential price of $3 per cwt, there is still a 10.8 percent chance of having a negative NPV (i.e., 100 – 89.2 = 10.8).

| Likelihood for positive net present value (NPV) | 89.2% |

|---|---|

| There is a 75% probability of getting an NPV ($/cwt) greater than … | $11.88 |

| There is a 50% probability of getting an NPV ($/cwt) greater than … | $25.62 |

| There is a 25% probability of getting an NPV ($/cwt) greater than … | $40.42 |

Resale Value of Milk Commission Base

As mentioned above, MCB is an asset that producers can resell, and therefore, it has a resale value. For example, a dairy producer owning MCB and quitting the dairy business can resell the MCB to another producer and recover part of the money previously invested. Despite this, the resale value of MCB at purchasing time is subject to uncertainty. For instance, how can a producer know, at the moment of purchasing MCB, how much it will cost in the future? It is possible that MCB will cost the same, more, or less money per cwt than what was paid when purchased. Also, it is a plausible scenario that the Virginia Milk Commission could cease to exist and MCB could then be worthless. To account for this possibility, the spreadsheet was developed to estimate the NPV of the investment, ignoring and considering the resale value of MCB. Depending on its purchase price, having a positive NPV relies more heavily on MCB resale value (fig. 5).

Conclusions

A simple decision-making tool utilizing net present value can be used to evaluate the expected profitability of purchasing Virginia MCB, taking into consideration the risk of such a decision. As seen in the break-even analysis, the purchasing cost of the MCB is the primary determinant of the NPV of the investment. In addition, the resale value of MCB determines NPV, especially when the purchasing cost of MCB increases. Farmers and consultants should consider the NPV for the investment, considering and ignoring the resale value of MCB before deciding on its purchase.

One final consideration is that all these analyses are pretax. Income taxes can affect net cash flows, thereby affecting the break-even timeline and the NPV. Also MCB does not depreciate as do other capital purchases. Producers should consult with a tax specialist before purchasing MCB.

References

Groover, G. 2009. The Income Side of Seasonal vs. Year-Round Pasture-Based Milk Production. Vir- ginia Cooperative Extension. Publication 404-113. http://pubs.ext.vt.edu/404/404-113/404-113.html.

Virginia Administrative Code. 2008. “Regulations for the Control and Supervision of Virginia’s Milk Industry.” 2VAC15-20-10. http://leg1.state.va.us/cgi-bin/legp504.exe?000+reg+2VAC15-20-10.

Virginia Cooperative Extension materials are available for public use, reprint, or citation without further permission, provided the use includes credit to the author and to Virginia Cooperative Extension, Virginia Tech, and Virginia State University.

Virginia Cooperative Extension is a partnership of Virginia Tech, Virginia State University, the U.S. Department of Agriculture (USDA), and local governments, and is an equal opportunity employer. For the full non-discrimination statement, please visit ext.vt.edu/accessibility.

Publication Date

February 14, 2023