Results of the 2022 Virginia’s Land Use-Value Assessment Program Survey

ID

448-257 (AAEC-304NP)

Acknowledgements

The authors would like to thank all the jurisdictions’ employees and constitutional officers who completed the surveys in a timely manner. Your cooperation improved the reliability and quality of the information reported.

Introduction

Virginia law provided for land use-value assessment for the preservation of real estate for agricultural, horticultural, forest, and open space use, deeming such to be in the public interest. Land use-value assessment serves to encourage proper use of real estate to assure sufficient agricultural, horticultural and forestal products; conserve natural resources and prevent soil erosion; protect water supplies; preserve open spaces; promote land use planning and orderly development; and promote a balanced economy and ease development pressures on rural land. 2 VAC 5-20-10. Fifty years ago, the Virginia General Assembly enacted this law to permit localities to adopt a program of special real estate assessments for agricultural, horticultural, forest, and open space lands. As lawmakers became aware of Virginia’s growing population, the implementation of land use-value assessment and programs to preserve undeveloped lands became a critical decision. Virginia is not the only state dealing with urban growth and development concerns. States across the nation are experiencing increased growth in urban centers, which are sprawling into undeveloped areas and putting pressure on rural landowners to sell their lands for development. Thus, state government has designed programs that allow localities to purchase and transfer development rights, donate conservation easements, and implement land use-value assessment.

Land use-value assessment, or the assessment of land based on its value in agricultural, horticultural and forestal “use,” is a common methodology for preserving lands. This procedure often reduces the tax burden for the landowner to mitigate development pressures. In accordance with Virginia Code Section 58.1-3230 et seq. provides,each jurisdiction may voluntarily enroll and implement this program at any point in time. Once a jurisdiction is enrolled, the constitutional officers and supporting staff are responsible for administering the program. In conjunction with the land use-value assessment program, Virginia also established the State Land Evaluation Advisory Council (SLEAC), which is directed to estimate the use-value of eligible land for each jurisdiction participating in the land use-value assessment program. Annually, SLEAC contracts with Virginia Tech’s Department of Agricultural and Applied Economics to develop an objective methodology for estimating the use-value of agricultural and horticultural lands and provide annual estimates for each participating jurisdiction.

Starting in 2003, SLEAC began conducting a survey every ten years among all commissioners of revenues and relevant constitutional officers in every locality to study the procedures and implementation used for the land use-value assessment program. The most recent survey was conducted between January and April of 2022. For a copy of the survey, please request through the LUVA contact page.

In conducting this survey, the purpose is to determine the following:

- Seek ways to improve the usefulness of agricultural and horticultural use-values.

- Capture how SLEAC estimates are being used by each jurisdiction.

- Understand how each jurisdiction implements and enforces their respective land use-value assessment program.

- Provide insights into how agricultural and forestry districts are administered.

- Understand how land in conservation easements is valued.

The survey, which contained 59 questions, was distributed among 133 counties and independent cities using an independently compiled list of Commissioners of the Revenue and assessing officers and shared through the Virginia Association of Assessing Officers (VAAO) listserv.

An email letter explaining the purpose of the survey and a link to complete the online survey was distributed in early March. After two weeks, follow-up emails were made to all localities who had not started or completed the survey. A week later, phone calls were made prioritizing those localities with known use-value ordinances. Lastly, a week before the survey deadline in early April, a final round of phone calls was made to jurisdictions with land use-value ordinances in place which had not started or completed the survey.

Of the 133 counties and cities the survey was distributed to, the program received 87 completed surveys, yielding a 65% participation rate. From the 87 completed surveys, 69% of the participants were from counties and 31% were from cities.

Land Use-Value Overview

Enrollment and Administration

Sixty-eight percent of the jurisdictions who participated in the survey indicated that their jurisdiction has an ordinance for land use-value assessment for property taxation. The results revealed that there were a variety of constitutional officers and/or supporting staff who completed the survey. Commissioners of the Revenue, Chief Deputies of Commissioners of the Revenue, city and county assessors, and real estate department directors were the most common local government officials to complete the survey. Individuals completing the survey had a range of nine months to 38 years of service. The median length of time on the job was 10 years.

Ordinance Submission

In accordance with Virginia Code, “any locality adopting an ordinance shall file a copy with the State Land Evaluation Advisory Council.” Since SLEAC is responsible for monitoring jurisdictions’ changes to the land use-value assessment ordinances, localities must report these documents to SLEAC. As a service to SLEAC and localities, ordinances were collected through the survey. Seventy-six percent of the 59 jurisdictions with land use-value programs provided their land use-value assessment ordinance through the survey.

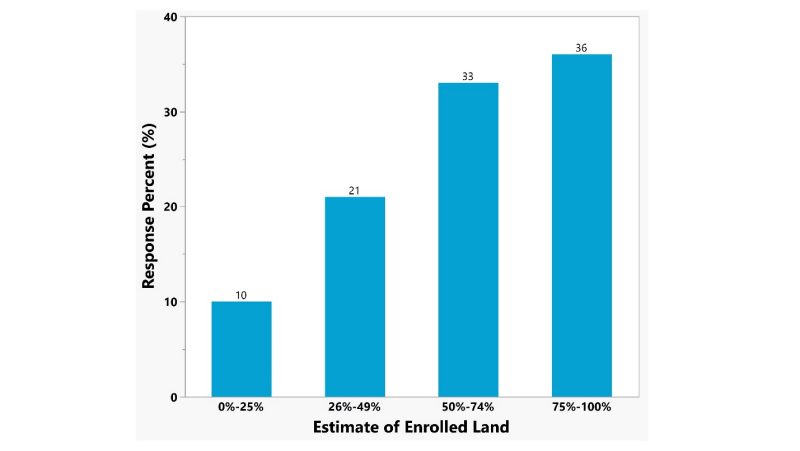

Eligible Land Enrolled

Respondents were asked to estimate the percentage of eligible agricultural and horticultural land in their jurisdiction that participates in the land use-value assessment program. As shown in Figure 1, 36% of localities believe that 75-100% of eligible land is enrolled, while 33% estimate that 50-74% of eligible land is enrolled.

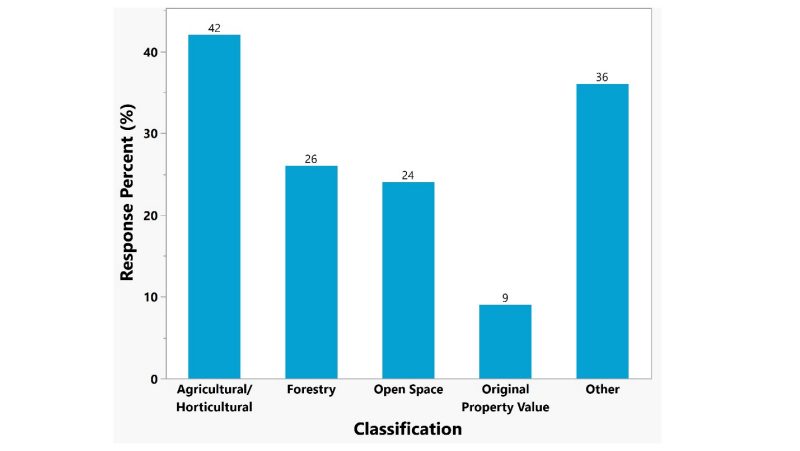

Conservation Easements

Eighty-four percent of respondents indicated that their jurisdiction has conservation easements. These jurisdictions were asked how the conservation easements are valued for tax purposes and a variety of responses were received. As depicted in Figure 2, 42% indicated that they value easements using the SLEAC values for agriculture and horticulture, while 36% of respondents indicated that they used “other.” For those answering “other,” a free response section was available for respondents to elaborate on how easements are valued within their jurisdiction. Responses indicated “other” conservation easement valuations are most commonly made on a case-by-case basis.

Land Use-Value Assessment

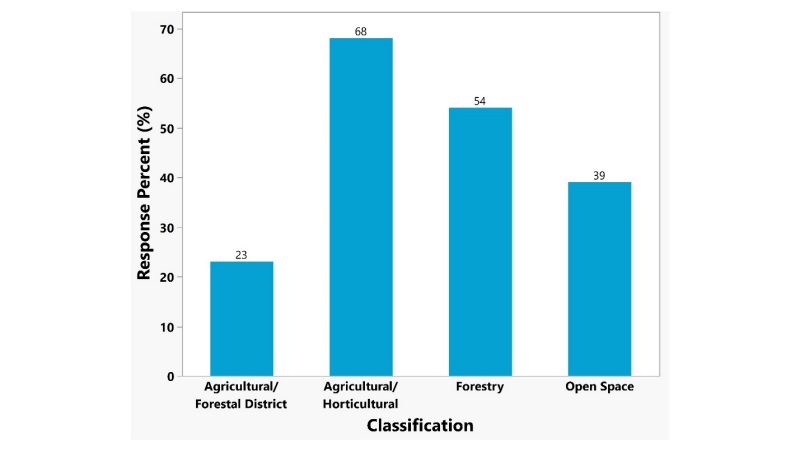

Depicted in Figure 3, 68% of the respondents indicated that their jurisdiction has a use-value ordinance and 23% have an agricultural/forestal district. Of those with a use-value ordinance, 68% have agricultural classifications, 54% have forestal classifications, 39% have open space classifications, and 53% have horticultural classifications. Notably, two jurisdictions, New Kent and Northampton, both have an agricultural and forest distract program although they have not enacted a land use-value assessment ordinance.

Eligibility and Verification

Regulation Change

Before reviewing the results of the eligibility and verification section, it is important to note that the Virginia Department of Agriculture and Consumer Services (VDACS) amended 2 VAC 5-20, Standards for Classification of Real Estate as Devoted to Agricultural Use and to Horticultural Use Under the Virginia Land Use Assessment Law, effective on October 15, 2020. The new amendments clarify eligibility requirements by listing the specified activities associated with agriculture and horticulture that must occur for the property to qualify as “real estate devoted to agriculture or horticulture use” and removed the then-existing minimum length of time requirement for eligibility, resolving a conflict between the Virginia Code and VDACS regulations.

Notable changes in the regulation affect the current use and exceptions of the property, the conservation of land resources, and the documentation of the certification procedures. The statute authorizing land use-value assessment did not change, however, the regulations modified for uniformity with the Virginia Code. For more information, please visit http://register.dls.virginia.gov/details.aspx?id=8183.

Eligibility Criteria

Once a locality adopts land use-value assessment, the constitutional officers are responsible for determining initial eligibility and monitoring the continued eligibility of land in the program. To receive insight into the application and revalidation process of the enrolled jurisdictions, respondents were asked a series of questions regarding eligibility determinations and validation procedures within their jurisdiction.

Jurisdictions were asked what criteria is used to distinguish bona fide operations for the purpose of eligibility. Table 1 lists the information required by participating jurisdictions and the four methods that received the greatest response percentage were:

- The number of acres the operation had devoted to production (97%).

- A copy of the owner’s IRS 1040-Schedule F (68%).

- A copy of the farm lease or affidavit from the tenant stating that the land is actively farmed (64%).

- The per acre number of animal unit-months of commercial livestock or poultry on the land (68%).

| Information Required | Application |

|---|---|

| The number of acres the operation has devoted to the production of agricultural, horticultural, or forestry products | 97% |

| A copy of the farm lease or an affidavit from the tenant stating the land is actively farmed | 64% |

| A timber management plan | 54% |

| An affidavit stating, for example, gross income, production, and/or management history, (crop yields, number of commercial livestock), dates and quantity of timber harvested, and so on | 47% |

| Whether or not the land has a planned program of soil management and soil conservation | 39% |

| Other | 22% |

| A copy of the owner's IRS 1040-Schedule F (farming) | 68% |

| The per acre number of animal unit-months of commercial livestock or poultry on the land | 64% |

| The number of consecutive years the land has been devoted to the production of agricultural, horticultural, or forestry products | 47% |

| Participation in local, state, or federal programs to improve/protect water quality and/or wildlife habitat | 41% |

| The crop yield per acre for each crop on the land relative to county average crop yields | 25% |

| A copy of the owner's IRS 1040-Schedule T (timber) | 17% |

Specialty Crops

A new area of interest for eligibility in the land use-value assessment program is with regards to specialty crops. In the Results of the 2012 Agricultural and Horticultural Use-Value Taxation Program Survey report, respondents with land use-value assessment programs and/or agricultural and forestal districts had no minimum acreage exceptions for specialty crops. However, in response to the 2022 survey, one county (Chesterfield) reported that it adopted an ordinance reducing the minimum acreage for specialty crops in the program, allowing a minimum of one acre for aquaculture.

Monitoring Enrolled Lands

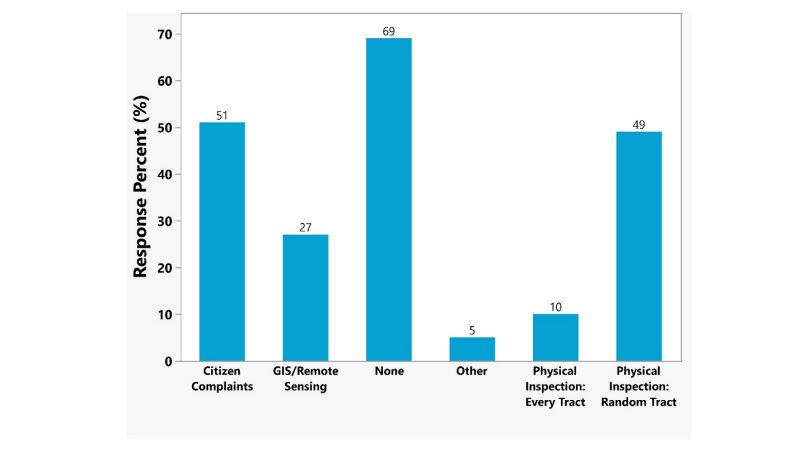

Respondents were asked what measures are undertaken to monitor enrolled lands to ensure that eligibility requirements are satisfied and to verify that the land is used for the bona fide production for sale of qualifying products or animals. As illustrated in Figure 4, the results indicate that the most common measures taken in 6 monitoring enrolled lands is a physical inspection of random tracts of participating land (49%), responding to citizen complaints (51%), or no measures undertaken at all (69%).

Non-Bona Fide Operations

Two questions were asked about non-bona fide operations for those enrolled in the program. First, the survey asked how many non-bona fide operations were identified in the locality within the past five years. The results indicated that 52% had zero non-bona fide operations, while 22% identified 1-10 non-bona fide operations enrolled. Correspondingly, when respondents were asked how many of the non-bona fide operations were penalized within the past five years, similar results followed. Seventy-six percent of respondents suggested that zero operations were penalized, while 17% of respondents reported that 1-10 operations were penalized.

SLEAC Land Use-Values

SLEAC Estimate Utilization

According to Virginia Code, the individual administering the program must “consider … the recommendations of value of real estate as such made by the State Land Evaluation Advisory Council” in establishing land use-values for their jurisdiction. Va. Code § 58.1-3236. To assess how localities use SLEAC values, respondents were asked whether they use the values “verbatim,” “as a major factor,” “as a minor factor,” or “not considered” in establishing land use-values for each classification of real estate. According to Table 2, the responses revealed that most localities either use the SLEAC estimates “verbatim” or “as a major factor” in establishing their rates for every classification of real estate.

| Classification | Used Verbatim | Major Factor | Minor Factor | Not Considered |

|---|---|---|---|---|

| Agricultural | 34% | 34% | 17% | 14% |

| Horticultural | 33% | 33% | 15% | 19% |

| Forestal | 23% | 34% | 11% | 32% |

| Open Space | 32% | 34% | 15% | 19% |

Note: The statistics represent the percentage of respondents with use-value programs for each classification.

Rental Rate Approach

Since 2010, SLEAC has approved the income and rental rate approaches to be used in supporting jurisdictions with estimated land use-values for all real estate classifications.

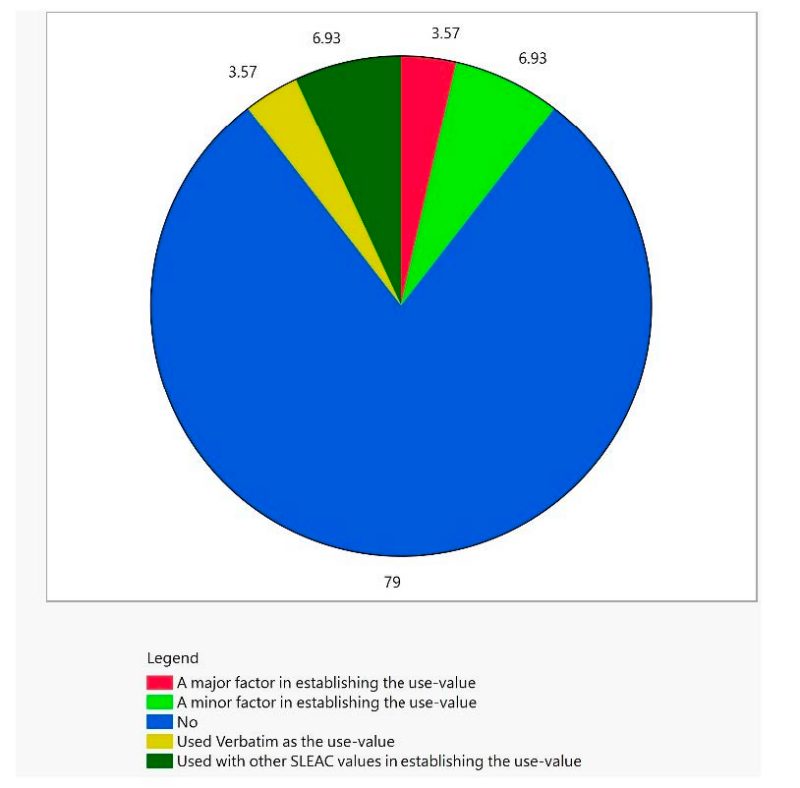

To assess whether localities are using the rental rate approach and estimates provided by SLEAC, the survey asked respondents whether they use the rental rate approach estimates for agricultural land. As shown in Figure 5, 79% percent of respondents indicated that they do not use the rental rate approach. The remaining 21% who indicated they do use the rental rate approach reported that the rental rate estimates are either a minor factor in establishing their rates or that they are used with other SLEAC values to establish their land use-values.

Most jurisdictions do not use the rental rate approach in establishing their land use-value estimates for agricultural and horticultural land. However, 36% of jurisdictions responded affirmatively when asked if they would consider using the rental rate approach in the future. This variance between the underused rental rate approach and interest in using rental rates in the future will require more research.

Assessed Value vs. Recommended Value

To assess the relationship between the actual assessed value and the SLEAC recommended value for agricultural and horticultural land, two questions were asked to determine whether the actual assessed values were lower, identical, or higher than the SLEAC values. The results indicate that roughly 60% of jurisdictions had actual assessed values higher than SLEAC recommended values and 20% of jurisdictions had assessed values that were lower than the SLEAC recommended values. For those respondents with assessed values that were higher or lower than SLEAC values, a follow-up question was asked to explain why its values differed. Several respondents opined that the SLEAC values were too low to meet the localities’ revenue needs.

Helpfulness of SLEAC Estimates

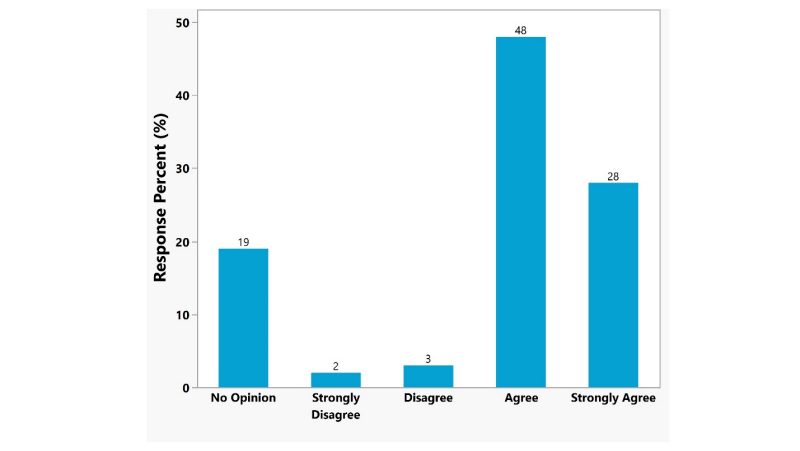

Jurisdictions were asked whether the annual SLEAC land use-value estimates of agricultural and horticultural land were helpful when assessing the land use-value of a participating land tract. Figure 6 depicts the jurisdiction’s level of agreement regarding the helpfulness of the SLEAC estimates when assessing the land use-value. Seventy-six percent of respondents either strongly agreed or agreed that the SLEAC estimates were helpful, 19% had no opinion, and 5% either disagreed or strongly disagreed.

Understanding of SLEAC Methodology

To gauge participating jurisdiction’s understanding of the SLEAC methodology for estimating the land use-values of all real estate classifications, the respondents were asked a series of questions on their level of agreement in understanding the estimates and making proper use of them. Table 3 lists the jurisdiction’s level of agreement regarding their understanding of SLEAC estimates and making proper use of the values.

For horticultural, forestal, and open space lands, most respondents either agreed or had no opinion regarding their understanding of SLEAC income approach use-value estimates. More than 40% agreed that their understanding is sufficient to properly use of the SLEAC estimates, while 42% had no opinion. Less than 10% of jurisdictions indicated that they did not have sufficient understanding of the methods and procedures for each off the three real estate classifications.

The degree of understanding was similar for agricultural land for the income approach and rental rate approaches. About 40% agreed that their understanding was sufficient to make proper use of the rental rate values, while 41% had no opinion.

| Opinion | Horticultural | Forestal | Open Space |

|---|---|---|---|

| Strongly Agree | 14% | 14% | 9% |

| Agree | 40% | 46% | 30% |

| Disagree | 4% | 5% | 7% |

| No Opinion | 42% | 35% | 54% |

Data and Available Resources

Land Capability Data

In this section, respondents were asked a series of questions regarding their usage of land capability classification data, and drainage characteristic data when assessing land use-values. First, survey participants were asked whether there was data available on the acreage in each Soil Conservation Services (“SCS”) land capability classifications for each and every individual land tract in their jurisdiction. If they responded affirmatively, a follow-up question asked whether such data is used in assessing land use-values. About 53% of respondents affirmed that there is data available on each SCS classification for their jurisdiction but only 22% use it to assess land-use values. For those who do not use the land capability classification data, another question followed asking why such data is not used in making assessment determinations. A few jurisdictions indicated that the information is not readily available and/or were unaware of the data resource.

Respondents were asked whether the SLEAC land use-value estimates for land that is at risk of flooding due to poor drainage is utilized when making use-value assessment determinations. Approximately 25% of respondents reported that they use the at-risk estimates when making assessment determinations. For those jurisdictions that do not, a follow-up question invited participants to elaborate on why at-risk values are not used. Of the responses received, jurisdictions indicated that those properties that are at high-risk for flooding are not enrolled in the land use-value assessment program. Lastly, only 25% of respondents indicated that there is data available for the drainage characteristics of each individual land tract in their jurisdiction. If this data was made available to them, only 22% of those jurisdictions reported that they would use it in making land use-value assessments.

Geographic Information Systems (GIS)

Many jurisdictions have GIS applications that overlay data for the purpose of tracking property values. These data can include wetlands, land capability classifications, soil types, agricultural and forestal districts, and more. To assess whether jurisdictions utilize GIS applications in their land assessment, respondents were asked a series of questions regarding GIS usage, the data layers employed, and whether there is interest in using GIS for tax assessment purposes.

When respondents were asked whether their jurisdiction employed GIS applications for determining soil classes and confirming land acreages, 57% responded affirmatively. For those jurisdictions, a second question followed asking them to explain what types of methods and data layers were utilized in their process. The responses were quite varied, and some noteworthy answers included using GIS to monitor construction, to manage easements, to map tree cover and wetlands, and monitor new properties enrolled in the program. Lastly, the survey asked localities whether they were interested in incorporating GIS applications into their property tax assessment methods. Fifty-three percent indicated that they were interested in utilizing these systems for tax assessment in the future.

Jurisdiction’s Perspectives

Program Effectiveness

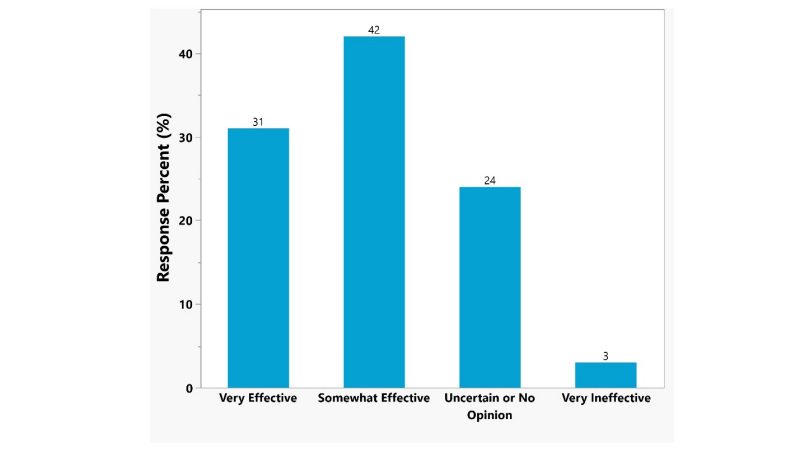

According to Virginia Law, the intent and one of the stated goals of the land use-value program is to ameliorate pressures which force the conversion of undeveloped land into more intensive uses. 2 VAC 5-20. To determine jurisdictions’ perceptions on the effectiveness of the program, the survey asked participants whether the land use-value assessment program is meeting the state’s goal in their jurisdiction. As shown in Figure 7, 73% supported the notion that the land use-value program is either very effective or somewhat effective in meeting this goal in their locality.

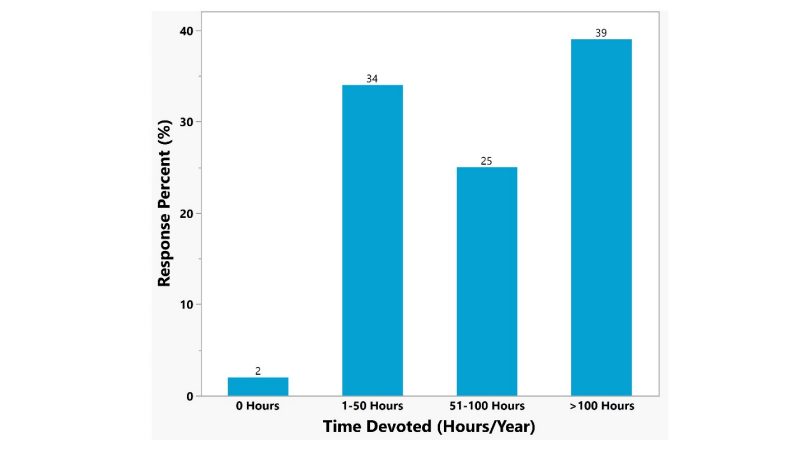

Time Devoted to Program

To evaluate the amount of time committed to the program, respondents were asked how many hours per year their staff dedicate to monitoring participating lands and ensuring that eligibility requirements are being met. Figure 8 shows the breakdown of hours per year that a jurisdiction’s staff devote to land use-value operations. Thirty-nine percent responded that their administrative staff dedicate 100 or more hours per year, while 25% dedicate 51-100 hours per year. Overall, about 65% of localities dedicate 51 hours or more per year in administering the program. Note, however, that these statistics greatly depend on the size of the locality’s land use-value assessment program and the locality’s administrative capacity. Localities considering a land use-value assessment program may anticipate hiring part-time or full-time employees to support administration of a new program.

Interest in an Online Seminar

Recognizing the administrative challenges of land use-value assessment programs, the survey aimed to gauge interest in future in-depth informative seminars regarding the SLEAC methods and procedures and general program administration questions. To the question of whether respondents are interested in attending an online seminar to learn more about the SLEAC methodologies, a total of 80% answered “Yes” or “Maybe.”

Frequently Asked Questions

To maintain current frequently asked questions (FAQs) for the LUVA website, the survey concluded with a space for respondents to list any questions or concerns that they have about the land use-value assessment program. Two jurisdictions suggested additional program materials and information. One request pertained to supplementing the SLEAC manual with additional guidance on handling the discontinuation of a qualifying use for land enrolled in the program, particularly regarding roll-back taxes. Furthermore, a request was made for additional training across the state for land use-value assessment administration with the coordination of Virginia’s Department of Taxation, VDACS, and the Virginia Department of Forestry. One jurisdiction requested that the SLEAC manual reinstitute apiary production under the animal units provisions, seeking additional information to effectively communicate with agricultural producers, including a growing beekeeper population.

Summary

Several conclusions can be drawn from the data collected during this survey about Virginia’s Land Use-Value Assessment program and SLEAC land use-value estimates.

The SLEAC values for agricultural, horticultural, forest, and open space lands are used by most localities either verbatim or as a major factor in determining their land use-value rates. While the SLEAC estimates are important in establishing a jurisdiction’s rates, each locality may alter these figures to accommodate unique characteristics within their jurisdiction. The number of properties enrolled, the economic climate, and the local government ordinances are common factors that drive whether the values increase or decrease. In most cases, the results indicated that jurisdictions are more likely to increase, rather than decrease, the land use-values above the SLEAC estimates because of continued pressure to maintain revenue streams, which may be a threat to continued program participation.

A majority of jurisdictions reported that the land use-value assessment program is effective in achieving its intended purpose and results indicated that most jurisdictions have a strong understanding of the program, though there is noteworthy interest in future informational seminars. Program administration regarding eligibility and verification vary widely, for which shared information amongst localities may prove to be a beneficial resource to localities looking to improve program administration.

Non-bona fide operations are a concern for many jurisdictions in the land use-value program. Within the past five years, about 20% of respondents reported that 1-10 non-bona fide operations had been identified and another 17% reported that 1-10 of the non-bona fide operations were penalized. To combat this issue, jurisdictions are taking various measures to monitor the participating lands to ensure eligibility requirements are being met. The most common measures include a physical inspection of random tracts of participating land (49%) and responding to citizen complaints (51%). Although non-bona fide operations are an inconvenience for jurisdictions, the survey results reveal that jurisdictions are monitoring participating lands and holding wrongdoers accountable.

The usage of land capability classification data and GIS applications has become more common for jurisdictions as they administer the use-value program. Nearly a quarter of respondents indicated that they use land capability classification data. Furthermore, more than half of participating jurisdictions utilize GIS applications for their property tax assessments. As the technology becomes more user-friendly and contains more powerful tools, the future of administering the use-value program may become more dependent on GIS technologies for data analysis, monitoring participating lands, and taxing tracts of land.

The SLEAC approved rental rate approach is underutilized by jurisdictions enrolled in the land use-value program. Nearly 80% of respondents indicated that they do not use the rental rate estimates. Intriguingly, more than a quarter of jurisdictions enrolled would be interested in using the rental rate estimates in the future. This contrariety will require more research to determine what barriers there are in using the rental rate approach estimates.

The survey results shed light on the variability of time commitment in administering the program. More than half of the enrolled localities dedicated less than 100 hours per year to monitoring participating lands and ensuring eligibility requirements are being met. The size of the locality and the number of properties enrolled greatly influence the amount of time necessary for program administration. More importantly, the administrative and financial capacity of the locality greatly impacts the amount of time and effort dedicated to the program.

In conclusion, this survey shows that land use-value assessment is a complementary part of the overall effort to manage agriculture, horticulture, forestry, and open space lands. All levels of government should continue exploring and developing comprehensive strategies to address the multitude of issues surrounding the support and protection of these lands through the land use-value assessment program.

Virginia Cooperative Extension materials are available for public use, reprint, or citation without further permission, provided the use includes credit to the author and to Virginia Cooperative Extension, Virginia Tech, and Virginia State University.

Virginia Cooperative Extension is a partnership of Virginia Tech, Virginia State University, the U.S. Department of Agriculture (USDA), and local governments, and is an equal opportunity employer. For the full non-discrimination statement, please visit ext.vt.edu/accessibility.

Publication Date

December 7, 2022